It’s late, the administrative department has already closed, and you’re still staring at an Excel file with too many tabs open. One contains invoices to be collected, another lists expected expenses, and yet another shows tax deadlines. The question, however, is always the same: will there be enough cash next month to pay salaries, suppliers, and perhaps fund a new business initiative?

For many Italian SMEs, cash flow management still works this way. They operate on an ad-hoc basis, relying on data from various sources, with payment cycles that aren’t always predictable and little visibility into what might change in two weeks. The result isn’t just stress. It’s a reactive approach to management that often slows down important decisions.

Meanwhile, the topic is moving beyond its niche status. By 2025, the global market for AI in accounting had reached $6.68 billion, with SMEs accounting for 68% of spending, according to this analysis of the AI market in accounting for SMEs. It is no longer a technology intended solely for large corporations with dedicated data science teams.

For an entrepreneur or an SME CFO, the point isn’t to chase the hype. The point is to understand whetherAI-powered cash flow forecasting for SMEs can truly lead to greater control, less manual work, and better decisions—especially in the Italian context of electronic invoicing, poorly integrated ERP systems, and budgets that are often closely monitored.

For many Italian SMEs, uncertainty doesn’t stem from a sudden crisis. It creeps into their daily routine. A payment that’s delayed by ten days, a supplier that needs to be paid sooner than expected, a tax form that’s more burdensome than last month’s, or a forecast that has to be quickly revised because three variables have changed in the meantime.

This is where spreadsheets reveal their limitations. They work as long as the data is limited, consistent, and stored in one place. In Italian business practice, this is often not the case. Some of the information is in the ERP system, some at the bank, some in the electronic invoicing system, and some in the accountant’s export files. Putting it all together takes time, and that time reduces the value of the forecast.

For SMEs, this issue is particularly significant. They make up the vast majority of the country’s business community and account for a large share of the national economy. When cash flow visibility is poor, the risk extends beyond just cash management. It leads to postponed orders, hiring freezes, strained relationships with suppliers, and a reduced ability to take advantage of incentives or grant programs, including those related to the PNRR.

In Italy, the point isn’t to adopt AI just because it’s trendy. The point is to determine whether a new tool can solve very real problems within companies that often start out with a lower level of digitalization than other European markets and with administrative processes that are still highly fragmented.

Without a reliable view of cash flows for the coming months, even a healthy company may postpone necessary decisions or err on the side of caution at the wrong time.

This is precisely why AI applied to cash flow forecasting is so valuable. It can help integrate various data sources, update forecasts more frequently, and flag discrepancies before they escalate into crises. It doesn’t eliminate uncertainty, nor does it replace the judgment of those who understand customers, seasonal trends, and payment habits. However, it provides business owners and financial managers with a more reliable foundation than manually updated files.

For an Italian SME, the right question isn’t whether the algorithm “predicts the future.” It’s much more practical. Can it effectively analyze the data I already have, including electronic invoicing data? Does it integrate with the systems I actually use? Does it help me make decisions a few weeks in advance, rather than just chasing my bank balance? The true value of the technology hinges on these questions.

At 8:30 in the morning, in many Italian SMEs, cash flow forecasting still begins with three screens open at once: online banking, the accounting software, and an Excel spreadsheet. Then the exceptions start to pop up. An electronic invoice that’s been issued but not yet collected. A customer paying outside the norm. A cost the purchasing department hadn’t reported. At that moment, the limitations of manual forecasting become clear. It offers a useful snapshot, but a static one, while the situation changes every day.

Cash flow forecasting with AI aims to bridge this very gap between operational speed and the slowness of traditional tools. In practice, it uses statistical and machine learning models to estimate future revenue and expenses based on historical and recent data, updating the forecast as inputs change. For an Italian SME, the key issue isn’t technical sophistication in and of itself. The key is whether the system can accurately interpret the data the company already generates—including electronic invoicing data—and transform it into a forecast credible enough to support concrete decisions.

In the traditional method, the finance team collects data, inputs assumptions, and builds a forecast that remains valid until actual conditions change. If expected cash inflows change or payment delays accumulate, a new manual step is required. This approach may suffice in simple companies with few transactions and regular cycles. It works much less well when cash flow depends on seasonality, customers with varying payment habits, closely spaced tax deadlines, and data spread across multiple systems.

An AI system works differently. It can link accounting records, bank transactions, schedules, sales data, and electronic invoices, then recalculate forecasts based on new signals. This is why the topic is of particular interest to Italian SMEs, where administrative data is often not stored in a single system, and part of the work still involves data exports, manual checks, or files shared with external consultants.

There is also a lesser-known aspect to this. Adoption does not depend solely on the quality of the algorithm. It depends on the quality of the company’s internal processes. If customer records, payment details, and accounting entries are inconsistent, even the best model will produce an unreliable forecast. If, on the other hand, the company has already streamlined its workflows—perhaps by leveraging incentives for digitalization or evaluating calls for proposals linked to the PNRR—the increase in utility can be much more rapid.

The acronym AI doesn’t refer to a machine that “predicts” the future. There are models that estimate probabilities based on patterns observed in the data. According to this explanation of ARIMA and gradient boosting models in cash flow forecasting, cash flow forecasting systems use approaches such as ARIMA and gradient boosting to analyze financial time series, identify relationships between revenues, costs, and payment times, and recognize trends, seasonality, and anomalies.

In practical terms:

A good forecasting system does not replace management judgment. It provides better and faster information to aid decision-making.

Why does it matter? Because it shifts the timing of the decision. If a company anticipates a slowdown in cash inflows, a spike in payments, or a period of tight liquidity, it has more options available. It can adjust purchase schedules, negotiate with customers and suppliers, postpone non-urgent expenses, or make investment decisions with greater clarity. For companies that are growing but remain financially unstructured, this foresight is often more valuable than a theoretically perfect forecast.

For many Italian SMEs, therefore, the value of AI forecasting does not lie in an abstract promise of accuracy. It lies in the shift from a document updated at regular intervals to a system that keeps pace with the company’s actual operations.

At 8:30 in the morning, in many Italian SMEs, the question is always the same: how much cash will we actually have in two weeks? The answer often comes from a hastily updated Excel spreadsheet, manually downloaded bank statements, and invoices scattered across different systems. In such a context, the benefit of AI is not theoretical. It is measured by the ability to spot a problem early and take action with multiple options on the table.

For an Italian business, this is even more critical. Those operating with tight margins, scattered cash flows, and compliance requirements like electronic invoicing know that cash flow rarely breaks down due to a single major event. More often than not, it deteriorates due to day-to-day friction: delayed payments, overlapping deadlines, and data scattered across management systems, online banking, and accounting software.

The most obvious benefit remains the quality of the forecast. In a summary published by Glean on cash flow management using AI, AI-based forecasting systems are associated with very high levels of accuracy—up to 95% in the best cases—and measurable financial improvements when forecasts become more reliable. The same source also highlights a significant structural fact: many companies operate with fragile cash reserves.

For an SME manager, precision means this: reducing the number of last-minute decisions. It means noticing early on when a major client is delaying payments. It means avoiding the situation where, at the end of the month, you realize that VAT, payroll, and supplier payments all fall due at the same time.

The difference is practical. A better forecast does not guarantee infallibility. It reduces avoidable errors.

In Italian companies, the benefits increase when the system also takes into account factors that are often overlooked. These include electronic invoicing deadlines, seasonal trends typical of certain sectors, the payment habits of repeat customers, and predictable expenses related to year-end bonuses, tax prepayments, or annual renewals. If these elements are incorporated into the model in an organized manner, the room for maneuver expands.

The second benefit becomes apparent in day-to-day operations. Many small and medium-sized businesses don’t just struggle because of a lack of foresight. They struggle because their administrative team spends too much time compiling data that already exists.

Anyone who manages cash flow knows this all too well. You have to check whether issued invoices have been entered into the right system, compare them with bank receipts, verify due dates, correct discrepancies, and send a new version of the file. If the company uses multiple tools, or if part of the process remains manual, the forecast arrives late and quickly becomes outdated.

With an AI system connected to operational data sources, the initial benefits are often clear right away. Less copy-and-pasting. Fewer repetitive reconciliations. More time to understand why the forecast is changing.

Forecasting that goes beyond just the final number. The team can focus on questions that truly impact the bottom line:

For Italian SMEs, this operational shift is particularly significant, as they often lack a large finance department. A single person may handle accounting, bank relations, tax deadlines, and management control. If the system reduces manual work, the benefits are felt immediately, even in small organizations.

The third benefit concerns the decision-making process. A forecast created solely to "check the balance" is only useful to a certain extent. An AI system becomes more valuable when it helps simulate concrete outcomes: What happens to cash flow if a customer pays 20 days late? What if the company brings forward purchases to protect itself from price increases? What if it opens a new store or hires two salespeople?

Here, the difference from the traditional method is clearly evident.

| Criterion | Traditional Forecasting (Excel) | Forecasting with AI (ELECTE) |

|---|---|---|

| Data Update | Manual and periodical | More continuous, based on updates and recalculation |

| Error Handling | It depends on who's looking | Automatic alerts and early warnings |

| Understanding Seasonality | Often simplified | Best suited for recurring patterns and variations |

| Scenario planning | Slow, handmade | Faster to simulate |

| Role of the Finance Team | Data collection and cleaning | Working Capital Analysis and Optimization |

A useful forecast doesn't just tell you "how much cash you'll have." It helps you understand which decisions are improving or worsening that trajectory.

For an Italian reader, there is another aspect to consider. Digital adoption among SMEs remains uneven, and for this very reason, the value does not come across through the sophisticated features listed in the brochure. It becomes apparent if the software integrates well with the company’s actual workflows: electronic invoicing, banking, ERP, scheduling, and accounting. And it becomes even more valuable if the company can incorporate the project into a broader investment strategy, for example by using PNRR incentives or other Industry 4.0 transition measures to cover part of the digitization costs.

There is also a more cautious view, and it deserves consideration. Not all companies have clean data. Not all have standardized processes. Not all are ready to rely on a predictive model right away. Some financial advisors point out that, without a solid accounting foundation, AI risks automating confusion rather than correcting it.

The objection is valid. But it does not invalidate the central point. In SMEs that start with clear objectives and carefully selected integrations, AI can transform cash management from a reactive task into an operational tool. It does not replace the judgment of the entrepreneur or the CFO. It simply enables them to make decisions sooner.

When a forecasting system works well, the types of figures that management reviews each week also change. They no longer just check the cash balance; instead, they examine the factors driving it.

The first set of KPIs pertains to working capital. This includes metrics such as DSO (average days sales outstanding), DPO (average days payable), and CCC (cash conversion cycle). Taken together, these metrics indicate how quickly the company converts operating activities into cash.

For those seeking a broader understanding of financial statements, it may be helpful to supplement these indicators with a guide to financial ratios and their analysis, so that cash flow is viewed not as an isolated figure but as part of a larger system.

A second group concerns the forecast time horizon:

According to this analysis of forecast automation and anomaly alerts, the direct integration of AI tools with bank feeds and invoicing systems eliminates the need for manual data entry and generates automatic alerts for critical anomalies, allowing finance teams to reallocate resources from repetitive tasks to strategic analysis and working capital optimization.

This also changes the way we interpret KPIs. They are no longer just numbers pulled at the end of the month. They become actionable insights.

For example:

Helpful tip: The best dashboard isn’t the one with the most charts. It’s the one that highlights three or four metrics that are truly relevant to your company’s decisions.

For a startup, the most critical metric may be the burn rate. For a retail business, the key issue may be the balance between inventory, cash receipts, and payments to suppliers. For a service company, the timeliness of collections by customer and by project is crucial. A robust AI system does not impose a one-size-fits-all approach. It must adapt to the company’s operational model.

When that happens, forecasting stops being a month-end task and becomes a dashboard to be used in meetings with sales, operations, and management.

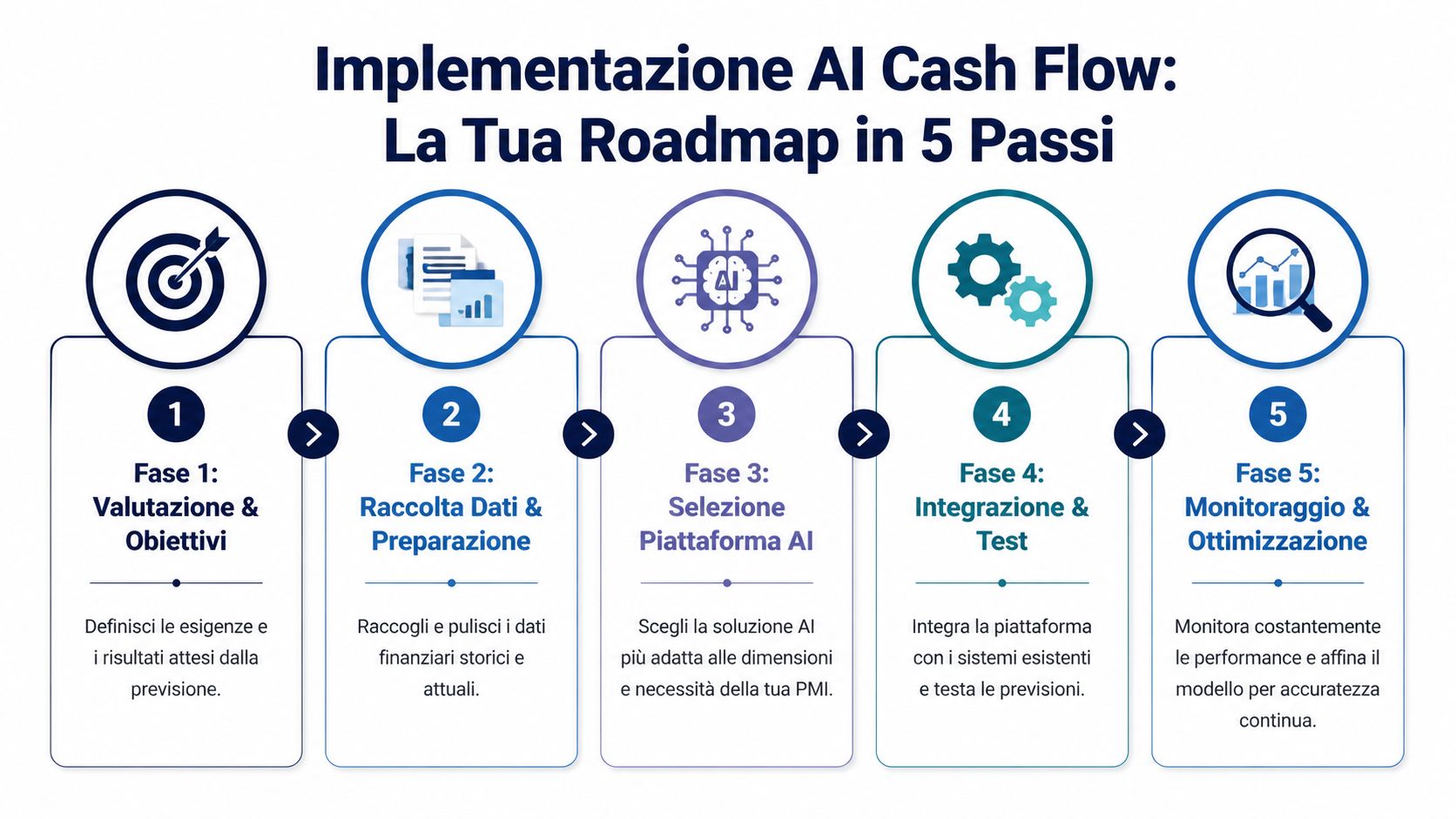

The most common obstacle isn’t technical. It’s mental. Many managers believe that implementing AI means undertaking a lengthy, costly, and unmanageable project for a lean organization. In reality, for small and medium-sized businesses, the process works best when treated as an incremental project with very concrete priorities.

1. Start with the problem, not the platform.

The initial question isn’t “Which software should we choose?” It’s “Where are we losing visibility today?” Some SMEs struggle with chronic payment delays, others with significant seasonality, and still others with too many disconnected systems.

2. Conduct a realistic assessment of the available data.

This is where the typical Italian friction often comes into play. Electronic invoicing, online banking, business management software, off-balance-sheet records, F24 forms, CRM: the data exists, but it isn’t always consistent or easy to integrate. Before discussing predictive models, it’s worth checking which sources are already accessible and which require minimal preparation.

If financial data is scattered, the first expected outcome isn’t a perfect forecast. It’s a more reliable database.

3. Evaluate the platform based on criteria specific to Italian SMEs.

According to this analysis of barriers to the adoption of financial AI in Italy, the main obstacles for Italian SMEs include annual costs ranging from €5,000 to €20,000, the fact that only 25% of SMEs have integrated ERP systems, and the need to integrate data from electronic invoicing and F24 forms. The same report highlights the role of platforms with scalable pricing and native integrations, even in the context of PNRR incentives.

It’s best to be very practical here. A platform may look great in a demo, but it won’t be very useful if it doesn’t integrate well with the data sources you actually use. That’s why it’s helpful to check in advance which data sources a system can connect to, especially if you work with different tools across administration, sales, and treasury.

4. Start small.

There’s no need to digitize your entire finance function all at once. It’s better to start with a clear use case—such as a 30- or 60-day forecast—for a limited set of cash flows. This helps you validate data quality, fine-tune rules, and determine which alerts are truly useful.

5. Make the rollout a management habit.

The project doesn’t end when the system goes live. The real value comes afterward, when forecasting becomes part of management routines. You need to compare forecasts with actual data, address exceptions, adjust drivers, and decide who uses which insights.

A sound workflow in small and medium-sized enterprises (SMEs) typically includes the following elements:

The adoption of AI-powered cash flow forecasting for SMEs is more likely to succeed when companies treat it as an operational discipline rather than a software purchase. It’s a subtle but crucial difference. The SMEs that derive value aren’t the ones that simply “install AI.” They’re the ones that integrate data, processes, and accountability in a way that’s simple enough to be sustainable over time.

For an Italian SME, the cases that really matter aren’t the ones that make for a good sales pitch. They’re the ones where the forecast helps determine whether to place an order early, follow up with a customer, postpone an expense, or use a line of credit only when necessary.

For Italian businesses, the starting point is often less theoretical than people think. The data already exists, but it’s scattered across accounting software, online banking, the accountant’s files, customer and supplier schedules, and electronic invoicing documents. The value of a predictive system becomes clear when it can bring these data streams together and translate them into a simple question: how much cash will we actually have in 15, 30, or 90 days?

In retail and e-commerce, the tension is well known. Too much inventory ties up cash flow. Too little inventory leads to stockouts and lost sales. A well-constructed forecast combines historical sales data, promotions, reorder lead times, returns, and expected cash receipts to show the financial impact of business decisions—not just their effect on revenue.

For a small chain or an Italian online retailer, one very practical factor also matters: local seasonality. Sales, November campaigns, pre-holiday spikes, and supplier delivery times all have an irregular impact on cash flow. A frequently updated model helps determine whether an aggressive campaign will actually increase available margin or whether it will tie up cash at exactly the wrong time.

In service companies, the problem takes on a different form. Inventory has little or no impact. What matters are late payments, advances on project costs, the differing behaviors of public and private clients, and contracts that appear profitable but result in slow cash flow.

Here, the forecast is used to identify customer patterns, not just sales figures.

A creative agency, a software company, or an engineering firm can use AI to estimate more accurately when an invoice will be paid, based on historical data regarding the customer, due date, amount, and time of year. For many Italian SMEs, this has a direct impact on payroll planning, VAT, and social security contributions. It also helps in dealings with the bank, as it provides a forecast that is less arbitrary and more verifiable.

In the Italian manufacturing sector, particularly among companies operating within long supply chains, working capital is the key issue. Raw materials, semi-finished goods, production lead times, logistical bottlenecks, advance payments to suppliers, and deferred collections all overlap. A spreadsheet often provides a snapshot of the month, but it struggles to track the delays that accumulate week after week.

The most practical use of AI in these situations is to anticipate potential issues. If a major order is delayed, if a supplier changes its terms, or if a long-standing customer extends payment terms, the system can estimate the impact on cash flow before the monthly closing. For a business owner, the difference is practical: renegotiating in time, adjusting purchases, or securing short-term financing in a more cost-effective way.

This type of assessment becomes even more important when a company is investing in digitalization or machinery, perhaps even with PNRR or Transizione 5.0 incentives. In such cases, it is not enough to know whether the investment is sustainable in theory. It is necessary to determine whether the cash outflow profile aligns with actual collection timelines and expected returns.

For a startup or a growing SME, the question changes again. The key issue is the runway, but also the quality of that runway. How much does a new hire impact cash flow? What happens if the go-to-market strategy costs more than expected? How much margin remains if a funding round is delayed or if an enterprise customer is 60 days late on payment?

Here, the forecast isn’t just useful internally. It’s useful externally as well. Investors, advisors, and financial institutions tend to have more confidence when the financial plan includes clear assumptions, regular updates, and well-explained variances.

In Italy, this also applies to many traditional companies that are launching a new digital initiative or an export channel. Growth creates needs before it generates cash flow. Anticipating these needs helps avoid hasty decisions.

In practice, the key difference lies in integration with existing processes. If the system doesn’t interface with electronic invoicing workflows, accounting, and banking data, the forecast remains incomplete. If, on the other hand, it can incorporate these elements in a structured way, it becomes a tool for day-to-day management, not just a task to be done at the end of the month.

To see how similar issues are addressed in different operational contexts, you may also find it helpful to consult this collection of case studies on analytics and forecasting for businesses.

The biggest mistake would be to portray AI forecasting as a frictionless shortcut. It isn’t. It works well when its limitations are recognized early on, not ignored.

The first risk is simple: if the input data is incomplete or inconsistent, the forecast will suffer as well. The classic “garbage in, garbage out” principle still holds true. Unreconciled invoices, unclassified bank transaction descriptions, duplicate customers, or poorly managed accounting processes all diminish the model’s value.

The second risk is cultural. Some managers expect the system to “know everything” right from the start. Others, on the contrary, are wary of it because they see it as a black box. Both positions create problems. A good model should be observed, compared with reality, and improved over time.

The third issue concerns the total cost. It’s not just about the subscription fee. Integration, internal time, potential external support, and data governance all play a role.

However, there are some very practical countermeasures:

Trust in predictive systems grows when people see how forecasts inform actual business decisions.

A word of caution is also in order. This article is for informational purposes only and does not constitute financial, tax, or legal advice. Every SME has a different cost structure, risk profile, and set of obligations. Before implementing a new system, it is advisable to assess your operational objectives, internal processes, and compliance requirements.

The key point is this: AI doesn’t make your business immune to uncertainty. However, it does make uncertainty easier to understand. And for an SME, that difference matters a great deal.

When forecasting is done manually, management spends time chasing numbers. When the process becomes more automated and predictive, that time can be redirected toward better priorities: safeguarding liquidity, evaluating an investment, anticipating customer risk, and planning for growth with greater precision.

AI-powered cash flow forecasting for SMEs makes the most sense here. Not as a tech fad, but as a decision-making framework best suited for businesses that need to act quickly with limited resources.

If your company is still mostly flying by the seat of its pants today, the solution isn’t to buy more technology. It’s about developing a more reliable outlook for the coming month—and then for the next quarter.

Yes, provided there is reasonably organized baseline data. In smaller businesses, automation is often even more valuable because the same person handles administration, collections, suppliers, and scheduling. If cash flows are irregular, even a simple but up-to-date forecast can make decision-making much easier.

The more consistent data you have, the better the system is at identifying patterns and seasonal trends. In practice, however, the point isn’t to have perfect datasets. It’s to have data that’s clean enough to generate a useful initial model. Then, the quality of the forecast improves as the system accumulates new signals and compares the forecast with actual data.

Security must be carefully evaluated, as with any platform that handles sensitive data. It is important to review GDPR policies, access procedures, permission management, encryption, and the structure of integrations. In general, the right question is not “Is AI secure?” but rather “Does this provider handle data in accordance with standards appropriate for our risk level and our obligations?”

No. A forecasting system generates alerts, scenarios, and automation. Decisions remain human. In the best SMEs, AI frees up time by handling repetitive tasks, allowing finance managers to focus more on priorities, exceptions, and corrective actions.

I usually start with a simple but concrete scenario: integrating key data sources, managing data flows in a more centralized manner, and creating a short-term forecast. In the Italian context, it makes sense to prioritize compatibility with electronic invoicing, ease of use, and the project’s cost-effectiveness.

If you want to move from spreadsheets to a more transparent and predictive approach to financial management, check out ELECTE, an AI-powered data analytics platform for small and medium-sized businesses. It’s a practical way to explore forecasting, automated insights, and data analysis without adding unnecessary complexity to your team.

.svg)

.svg)

.svg)