Financial statement analysis using ratios is the process of transforming raw financial data—such as that from the balance sheet and income statement—into simple, easily understandable indicators. In short, it is the art of letting the numbers speak for themselves so you can instantly grasp the health of your business: its liquidity, financial strength, profitability, and efficiency.

In this guide, we’ll walk you through the process step by step. The goal is to transform complex calculations into practical, actionable insights. You’ll learn how to interpret key financial and economic indicators so you’re no longer overwhelmed by numbers, but can start using them to your advantage to make faster, smarter decisions.

Every SME owner constantly faces a dilemma: should they trust their instincts or rely on data? All too often, financial statements are seen as a tedious tax obligation—a pile of numbers to hand over to the accountant and then file away until the following year.

What if those numbers could tell the story of your company, revealing its strengths and, more importantly, flagging potential issues before they turn into emergencies?

This is wherefinancial statement analysis using ratios comes into play—a methodology that transforms cold, static accounting data into a true strategic compass for navigating the market.

The idea that financial analysis is the exclusive domain of expert analysts or multinational corporations is a myth that has long since been debunked. Today, thanks to accessible platforms, these indicators are an essential tool for any manager or entrepreneur who wants to make decisions based on facts, not gut feelings.

Thinking of your financial statements solely in terms of taxes is like having a treasure map and using it as a coaster for your coffee cup. Hidden within those documents are the answers you’re looking for to grow your business.

The goal of ratio analysis is not merely to "interpret" the past, but to use that knowledge to build a more solid and profitable future. It serves as the bridge connecting accounting to strategy.

Thanks to this process, you can finally get clear answers to questions that are critical to your business:

Often, the first step is simply to get the data into a usable format; in this regard, you might find our guide on how to convert PDF files into Excel spreadsheets helpful.

Think of your business as a ship sailing the seas of the market. To navigate safely, you need two essential things: enough fuel for the immediate journey ( liquidity) and a sturdy hull to withstand unexpected storms ( financial strength).

Liquidity refers to your business’s ability to meet immediate financial obligations, such as paying salaries, suppliers, and taxes. Solvency, on the other hand, concerns the long-term balance between your assets and liabilities, determining the company’s structural resilience in the face of economic shocks.

These aren’t abstract concepts. They can be accurately measured throughfinancial statement analysis using ratios, turning numbers into a strategic compass. Let’s take a look at the key indicators for assessing the financial health of your small business.

Liquidity ratios answer a very practical question: "If I had to pay off all my short-term debts today, would I have enough assets that could be easily converted into cash to do so?" They serve as the first, crucial warning sign for preventing cash flow crises.

The two most commonly used ratios are the current ratio and the quick ratio.

This ratio compares current assets (cash, accounts receivable, inventory) with current liabilities (accounts payable, short-term tax liabilities, upcoming mortgage payments).

Its formula is straightforward:Current Ratio = Current Assets / Current Liabilities

A ratio above 1.5 is generally a good sign. It means that, for every euro of short-term debt, you have at least 1.5 euros in readily liquid assets to cover it. If it falls below 1, that’s a serious cause for concern.

The Quick Ratio is a more conservative version of the Current Ratio. The reasoning behind it is simple: inventory might not be so easy to sell quickly without having to sell it at a loss. For this reason, it excludes inventory from the calculation.

The formula becomes:Quick Ratio = (Current Assets - Inventories) / Current Liabilities

This ratio tells you whether you can pay off your short-term debts using only your most liquid assets. A value greater than 1 is considered optimal, because it means you can cover all your immediate obligations without having to dip into inventory.

Practical example: A company has €200,000 in current assets (including €80,000 in inventory) and €120,000 in current liabilities.

- Current Ratio: 200,000 / 120,000 = 1.67 (Positive)

- Quick Ratio: (200,000 - 80,000) / 120,000 = 1.0 (Balanced, but worth keeping an eye on)

If liquidity is the fuel, financial strength is the ship’s structure. These ratios measure how much your company relies on external capital relative to its own resources. Excessive reliance on debt makes it more vulnerable to rising interest rates or a credit crunch.

This is the key indicator of financial strength. It compares the company’s total liabilities with its equity.

The formula is:Leverage = Total Liabilities / Net Assets

This figure tells you how many euros of debt you have accumulated for every euro of capital invested by shareholders.

A recent analysis has shown that Italian corporations have strengthened their financial structure. According to the data, the equity ratio improved, rising from 43.9% in 2022 to 45.4% in 2023, a sign of their growing ability to self-finance. You can explore these figures in more detail in the Italian Corporate Financial Statements Observatory.

To keep formulas and definitions handy, here’s a summary table that you might find useful.

A summary table for quickly calculating and interpreting key liquidity and capital adequacy ratios, along with their ideal benchmark values.

Always remember that these ratios, however fundamental they may be, should never be interpreted in isolation. Their true value becomes apparent when you analyze them over time and compare them to the average for your industry. Only then doesfinancial statement analysis using ratios transform from a simple numerical exercise into a powerful tool for strategic decision-making.

A company may be financially sound and have cash on hand, but if it doesn’t generate profits, it’s like a powerful engine idling at a traffic light: it’s not going anywhere. Profitability ratios serve as the dashboard that measures that engine’s efficiency, answering the most important question of all: is the capital you’ve invested generating real value?

While liquidity and solvency ratios ensure that your business is staying afloat, profitability ratios verify that it is also capable of thriving.Financial statement analysis using profitabilityratios allows you to understand not only whether you are making a profit, but more importantly, how and where you can increase your profits.

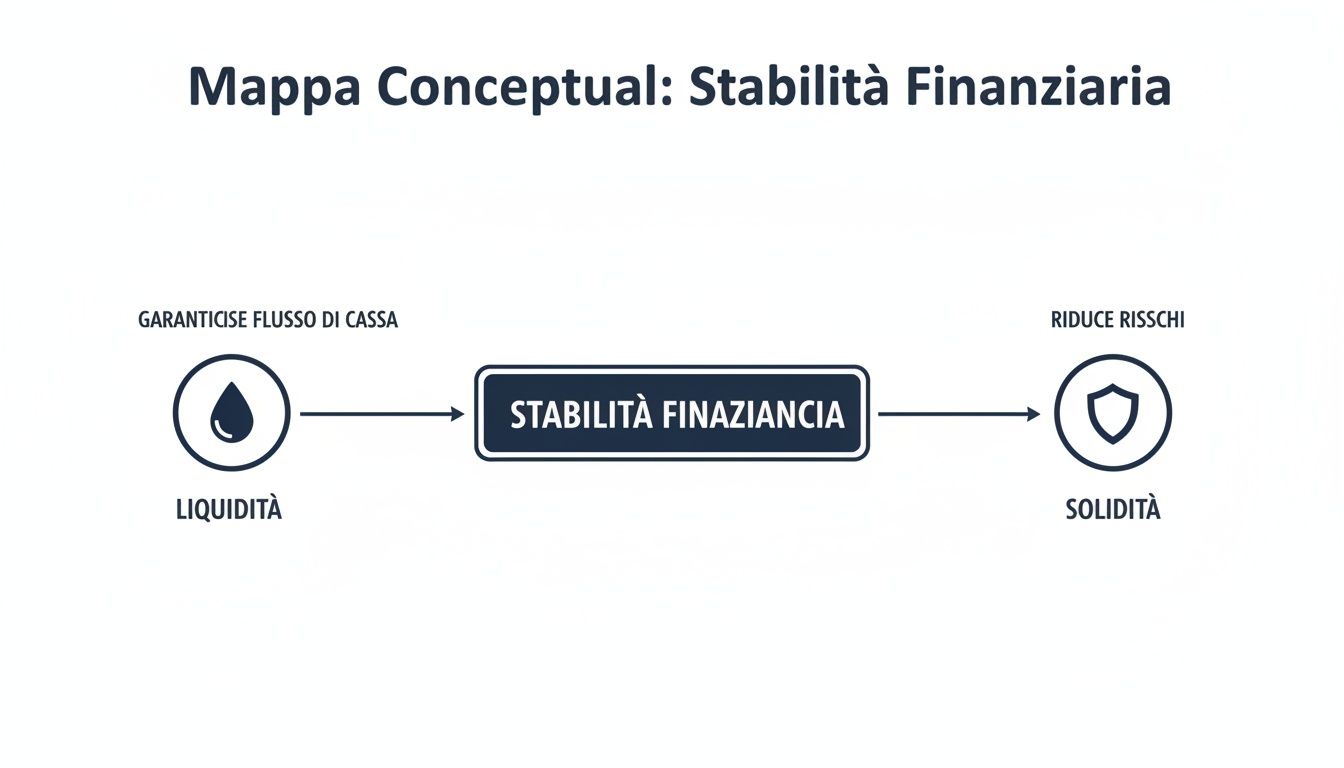

The map below illustrates this concept well: liquidity and financial strength—which we’ve already discussed—form the foundation. Only on a solid foundation can we build long-term profitability.

This image reminds us that only a financially stable company, with strong cash flow and a solid balance sheet, can truly aim for sustainable profitability.

Return on Equity (ROE) is perhaps the metric most closely watched by shareholders and investors. Its purpose is clear and straightforward: to measure how much return is generated by every single euro of equity invested in the company.

The formula is simple:ROE = Net Profit / Shareholders' Equity

A high ROE is a strong indicator: the company is creating wealth for its investors. For example, an ROE of 15% means that for every 100 euros invested by shareholders, your company has generated 15 euros in net profit.

But be careful. A very high ROE can sometimes hide a catch: high debt (the so-called "financial leverage"). If a company relies heavily on debt to finance its operations, its equity decreases and the ROE is artificially "inflated." That’s why it should always be analyzed in conjunction with other ratios.

Return on Investment (ROI) shifts the focus from profitability for shareholders to overall management efficiency. In practice, it tells us how well your company generates profit from the total capital invested, whether it comes from shareholders or banks.

Here's how to calculate it:ROI = Operating Profit (EBIT) / Total Capital Invested

ROI shows you how effectively you’re using your resources (machinery, warehouses, raw materials) to generate revenue, regardless of how much you paid for them. It’s the true barometer of your core business’s performance.

Practical example: A company with a 10% ROI and a cost of debt of 4% is creating value. It’s simple: it earns more than it costs to finance itself. If the ROI dropped to 3%, the situation would be reversed: the company would be destroying value. For more information, check out our practical guide to net invested capital.

A healthy and stable ROI over time is one of the surest signs of efficient and well-managed business operations.

Finally, Return on Sales (ROS) goes into even greater detail. It focuses on a company’s ability to convert revenue into profit. This metric measures the percentage of operating profit remaining from every euro of sales.

Here is the formula:ROS = Operating Profit (EBIT) / Sales Revenue

An operating margin of 12% means that for every 100 euros of products or services sold, your company retains 12 euros in operating profit after paying all production and operating costs.

It is a key indicator for determining whether you are competitive in the market and whether your pricing strategies are effective. A declining ROS, for example, may signal that margins are being squeezed by the competition or that costs are spiraling out of control.

Ultimately, that is the purpose of financial analysis: to uncover a company’s true efficiency. But analysis for its own sake is not enough; the goal is always to improve—for example, by learning how to maximize profits in the management of a lodging facility.

The true powerof financial statement analysis using ratios becomes apparent when you look at these three indicators—ROE, ROI, and ROS—together, as if they were telling a story.

Using these three metrics together gives you a comprehensive view of your company’s performance. It transforms simple numbers into a detailed roadmap to guide your strategic decisions toward profitable and sustainable growth.

If profitability is the engine of your business, cash flow is the fuel that keeps it running every day. It’s not uncommon to see companies that are profitable on paper go under due to a cash crunch. That’s whyfinancial statement analysis using turnoverratios is essential: it shifts the focus from “how much you’re earning” to “how quickly you’re collecting payments.”

This set of metrics doesn’t measure profit, but rather how efficiently you manage day-to-day operations. In other words, they tell you how quickly you can turn your resources—such as inventory or accounts receivable—into cash. An old adage in finance goes: “Profit is an opinion; cash is a fact.” These indicators are the tools for turning this maxim into a concrete strategy.

For many small and medium-sized businesses, inventory is one of the biggest investments. And idle inventory is, in effect, money tied up that isn’t working for you. The inventory turnover ratio measures exactly that: how many times a year you are able to sell and completely restock everything you have on the shelves.

The formula is simple:Inventory Turnover Ratio = Cost of Goods Sold / Average Inventory

A high figure is a very good sign: your products are moving, and sales are strong. A low figure, on the other hand, is a red flag. It could mean you have obsolete inventory, an ineffective purchasing policy, or—worse yet—products that the market no longer wants.

This metric forces you to ask yourself some critical questions: Am I tying up too much cash in inventory? Which products are slowing down my cash flow? Is my purchasing policy aligned with actual customer demand?

For an even more concrete figure, you can calculate its twin: the average days in inventory.Days in Stock = 365 / Inventory Turnover Ratio

This figure tells you, on average, how many days an item sits in inventory before being sold. The goal? To minimize this time, of course without running the risk of running out of stock for customers.

There are two extremely powerful—and often underestimated—tools for managing cash flow: accounts receivable and accounts payable. Taking proactive steps on these two fronts can free up vital resources without having to turn to the bank.

DSO is a metric that measures the average amount of time that elapses between when you issue an invoice and when the funds actually appear in your account. Needless to say, a low DSO is a sign of excellent financial health.

DSO = (Trade Receivables / Sales Revenue) * 365

Every single day you can shave off your collection cycle translates into immediate cash flow for your business. If your DSO is 60 days, that means you’re effectively financing your customers for two months. Reducing it to 50 days can make a huge difference in your bank account.

Similar to the DSO, the DPO measures the average time it takes your company to pay its suppliers.

DPO = (Trade Payables / Cost of Goods Sold) * 365

Here, the situation is reversed. A longer payment term—while still adhering to agreements and maintaining good relationships with partners—allows you to keep cash on hand longer, using it to finance operations.

Let’s put the pieces together. By combining these three metrics, we arrive at the Cash Conversion Cycle (CCC). This figure, expressed in days, tells you how long it takes your company to turn its investment in inventory and other resources into actual cash.

The formula summarizes the flow of money:CCC = Days in Stock (inventory) + Days Sales Outstanding (DSO) - Days Payable Outstanding (DPO)

Let's look at a practical example:

Your cash cycle will be: CCC = 45 + 60 - 30 = 75 days.

What does that mean? It means that your company has to be self-financing for 75 days. In other words, it has to cover all operating expenses (salaries, rent, utility bills) before seeing any revenue from sales. Shortening this cycle—even by just a few days—has a direct and incredibly positive impact on your available cash flow.

Financial statement analysis using turnoverratios is not merely an accounting exercise. It serves as the true control panel for optimizing working capital and ensuring that operational efficiency translates into healthy, solid, and financially sustainable growth.

Calculating your company’s ratios is an excellent first step. But it’s a bit like knowing how fast you’re running without knowing whether you’re in a sprint or a marathon. A number on its own, no matter how precise, lacks context.Financial statement analysis using ratios only becomes truly powerful when we start making comparisons, pitting that number against two key factors: your past performance and your competitors.

It is precisely through comparison that true value emerges. Let’s take a look at two fundamental techniques for transforming raw data into strategic insights: historical analysis and industry benchmarking. These two approaches will help you understand not only “where you stand,” but also “how you got there” and “how you compare to others.”

The first—and perhaps most important—form of comparison is the one you make with yourself. Historical analysis simply involves comparing today’s financial ratios with those of previous years. This exercise may seem trivial, but it can actually reveal trends, dynamics, and warning signs that a single-year analysis would completely overlook.

An ROI that drops from 12% to 9% over three years isn’t just a decline—it’s a red flag signaling a likely structural efficiency problem. Conversely, a current ratio that steadily improves indicates increasingly careful and sound liquidity management.

This analysis helps you answer questions that are crucial to your strategy:

Comparing data over time transforms a static snapshot of a single financial statement into a dynamic snapshot of your company’s performance. It helps you understand the direction you’re heading in and make course corrections before it’s too late.

While historical analysis tells you how you're performing compared to your past, benchmarking tells you how you're performing compared to the rest of the world. In practice, this involves comparing your metrics to the averages in your industry.

Are you more or less profitable than your direct competitors? Are your collection times in line with market standards? Without these comparisons, you risk celebrating a 5% ROE when the industry average is 15%, or worrying about inventory that turns over four times a year when the norm for your competitors is three.

Fortunately, finding this data is no longer an impossible task. Authoritative sources such as chambers of commerce, trade associations, and platforms specializing in financial analysis provide aggregated data by sector (ATECO code) that you can use as a reference point.

Using benchmarks allows you to:

By combining historical analysis and benchmarking,financial ratio analysis ceases to be a dry accounting exercise. It becomes a powerful tool for competitive intelligence, capable of transforming simple numbers into a clear strategic advantage for your small business.

Anyone who has spent hours on a spreadsheet analyzing financial statements knows the drill: it’s a slow, repetitive process riddled with pitfalls. All it takes is one incorrectly entered data point or a formula that doesn’t update to undo hours of work. That’s precious time you could have spent on strategy, not filling in cells.

Fortunately, there is now a smarter and faster way.

AI-powered data analytics platforms, such as ELECTE, are revolutionizingfinancial statement analysis using key ratios for small and medium-sized enterprises (SMEs). Say goodbye to manual work. These systems connect directly to your data sources—such as your ERP system or accounting files—and calculate dozens of key ratios in real time.

The real leap forward isn't just about speed—it's about clarity. Instead of getting lost in a maze of numbers and formulas, you have interactive dashboards right in front of you that show you the health of your business at a glance.

In short, these platforms allow you to:

This transforms financial statement analysis from a periodic, laborious task into a continuous monitoring process—almost like a strategic co-pilot for your company.

The point isn't to get data entry done faster. It's to free up your time so you can focus on what really matters: interpreting insights to make better decisions, faster.

But the real turning point comes when you stop looking only to the past. The most advanced platforms use artificial intelligence not only to assess the current situation, but also to anticipate what might happen tomorrow.

An AI system can analyze your historical cash flow data and your customers’ payment habits. The result? An accurate forecast of any potential cash flow issues in the coming months. Having this information allows you to take proactive steps, rather than reacting once the problem has already arisen.

Automation, therefore, is not just a matter of efficiency. It is a genuine strategic advantage. It provides SMEs with analytical tools that, until recently, were a luxury reserved only for large corporations.

If you want to better understand how these systems work and how they can help boost your growth, you can read our in-depth article on Business Intelligence software.

We’ve seen how financial statement analysis using ratios can turn your accounting data into a strategic compass. Here are 4 key steps to start using this information right away to grow your business.

Financial statement analysis using ratios isn’t just a theoretical exercise—it’s the most powerful tool you have for making informed decisions and steering your small business toward a successful future. Turning raw data into clear insights allows you to anticipate problems, seize opportunities, and optimize your resources with precision.

Today, thanks to AI-powered platforms like ELECTE, you no longer need to be a financial expert to reap these benefits. You can automate calculations, view your KPIs on intuitive dashboards, and free up valuable time to focus on strategy. It’s time to stop viewing your financial statements as a chore and start seeing them as your best ally for growth.

Are you ready to turn numbers into strategic decisions, without the hassle of spreadsheets? Find out how ELECTE help you grow and start making smarter decisions today.

.svg)

.svg)

.svg)