This is a familiar scenario in many small and medium-sized businesses. The administrative team is scrambling to complete last-minute reconciliations, the board of directors is waiting for the final documents, the auditor is requesting clarification on certain items, and, in the meantime, the date of the shareholders’ meeting is fast approaching. At that point,getting the financial statements approved feels like a race against time.

That is an oversimplified view. The approval of the financial statements is not merely the final step in fulfilling a legal requirement. It is the point at which a company makes its financial position and economic performance transparent to shareholders, creditors, and other stakeholders. If the process is delayed or mishandled, the problem is not confined to the corporate secretariat. It affects governance, banking relationships, profit distribution, and the ability to make decisions.

That’s why it’s worth shifting your perspective. Don’t start by asking, “When is the deadline?”, but rather a more useful question: “How do I structure the process to avoid a last-minute rush?” The rules remain central, but the real operational difference lies in data preparation, clarity of roles, and the ability to prevent bottlenecks before they turn into delays.

Anxiety often stems from a misunderstanding. People tend to think thatthe approval of the budget is an event that takes place over just a few weeks, whereas in reality it is the result of a process that should unfold throughout the year.

When this process is poorly managed, the final days become a hotbed of various problems. Incomplete accounting data, delayed document reviews, reports submitted late, and meetings squeezed into a tight schedule. The result is an organization that operates in a reactive, unmanaged manner.

Italian corporate law has long treated financial statements with this level of seriousness. The evolution of the law, which began with the Commercial Code of 1882 and was later codified in the Civil Code of 1942, follows a clear path: financial statements are not merely a means of closing the books, but are intended to ensure clarity, accuracy, and transparency in the presentation of the company.

For an SME, this has concrete implications. The approval of the financial statements must be managed as an operational risk process. Those who treat it as a mere formality tend to notice problems too late. Those who treat it as a structured process gain greater control, experience less internal friction, and make better decisions.

The approval of the financial statements is the resolution by which the shareholders review and approve the financial statements prepared by the directors. From a legal standpoint, it is a mandatory step. From a managerial standpoint, it is a test of the quality of governance.

Historically, this issue did not originate as a mere bureaucratic formality. The evolution of Italian regulations began with the Commercial Code of 1882, reached a turning point with the Civil Code of 1942—which formally introduced the balance sheet, income statement, and notes to the financial statements—and was brought into line with European standards by Legislative Decree 139/2015, which transposed EU Directive 34/2013. This process affects over 1 million corporations registered in Italy, as outlined in the slides on the historical and regulatory evolution of financial statements.

This historical fact leads to a practical conclusion. The legislature has gradually transformed the financial statements from a simple accounting document into a tool for economic and financial communication. For an SME, approving them properly and on time means lending credibility to its corporate narrative.

Many entrepreneurs focus on the final signature. In reality, approval indicates whether the company is capable of:

A properly approved financial statement does more than just ensure compliance. It helps reduce doubts, requests for clarification, and friction in dealings with those who assess the company’s financial health.

There is also a less-discussed aspect. The approval of the budget is one of the few occasions when company management is forced to compare the company’s internal narrative with its official presentation.

If you want to review the structure of the document before proceeding with the shareholders’ meeting process, a guide to the annual financial statements may be helpful.

This is why compliance becomes a strategic priority. If delays, controversial issues, or incomplete documentation arise, the problem is not merely technical. It points to weaknesses in the company’s information systems, in coordination between departments, and in its ability to effectively close out its decision-making process.

The regulations may seem complex, but when it comes to the day-to-day management of corporations, the key point is simple: there are strict deadlines and a precise sequence of requirements. If one step is skipped, it creates pressure on the subsequent ones.

According to Article 2423 of the Civil Code, the statutory deadline for approving the financial statements is a predetermined period following the end of the fiscal year. For the fiscal year ending December 31, 2025, the shareholders’ meeting must approve the financial statements by April 30, 2026. In exceptional cases, an extension to a longer period moves the deadline to June 29, 2026. Filing with the Business Registry must be completed shortly after approval, therefore by May 30, 2026, or by July 31, 2026 in the event of an extension, as summarized by Datalog Italia regarding the approval of financial statements.

These dates are not just a formality. They define the safety parameters within which the process must operate.

The provisions most frequently cited in practice are Article 2423 of the Civil Code regarding the preparation of financial statements, and Articles 2364 and 2478-bis of the Civil Code regarding the governance of general meetings for joint-stock companies (S.p.A.) and limited liability companies (S.r.l.). This gives rise to a concrete chain of liability.

| Actor | Main responsibility | Operational implications |

|---|---|---|

| Directors | They prepare the draft budget | They must initiate the process in a timely manner and coordinate the flow of information |

| Audit Committee | It ensures, where applicable, compliance with the rules and the adequacy of the structures | Requires complete and timely documentation |

| Statutory auditor | Submit a report, if appointed | It needs actual, uncompressed processing times |

| Annual General Meeting | Approve the budget | Decide based on accessible and accurate documentation |

| Business Registry | Receives the final payment | This completes the final step of the process |

The timeline exists for a specific reason. It serves to ensure:

If the company’s internal schedule aligns with the legal deadline only in the final weeks, the risk does not stem from the regulation itself. It stems from the fact that the company started too late.

The extension to 180 days should not be viewed as a convenient automatic extension. It is an exception that should be applied only when the specified conditions are met, such as in the exceptional cases provided for under civil law.

From an operational standpoint, the extension can provide some breathing room. But if it is used to compensate for disorganization, it does not solve the problem. It merely postpones it. A well-structured SME uses the extra time to manage real complexities, not to delay tasks it could have started earlier.

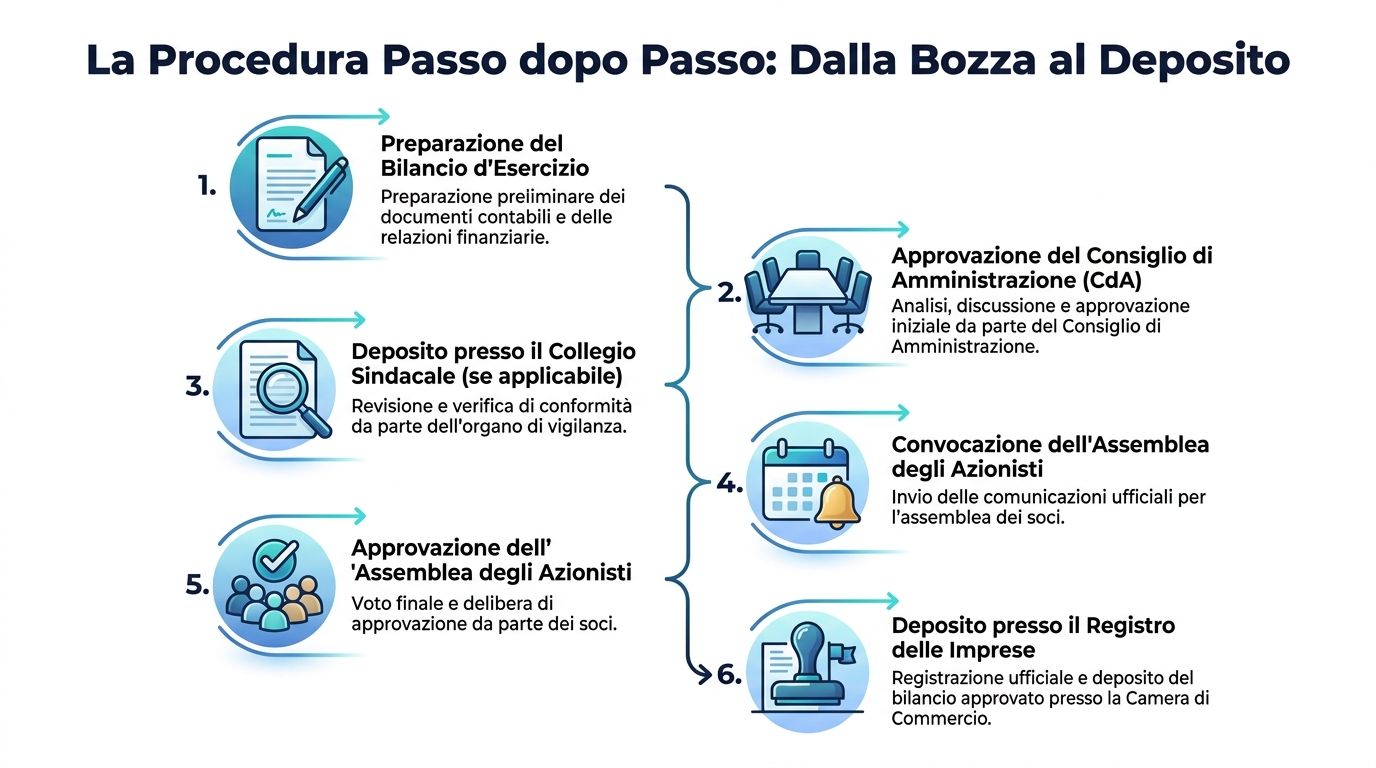

The most common mistake is to treatthe approval of the budget as if it depended solely on the administrative department. That is not the case. The process works when each corporate body takes action at the right time, within a clearly defined scope.

The board of directors bears primary responsibility. It prepares the draft financial statements and oversees their overall structure. Its role is not limited to compiling figures; it must ensure that the items accurately reflect the company’s financial position.

This point has very practical implications. If management and the finance department only meet right before the final draft is ready, the process starts off on the wrong foot. The most sensitive decisions require early discussion, not rushed approval.

When in place, the supervisory body ensures compliance with administrative rules and the proper conduct of procedures. The statutory auditor, if appointed, issues a professional opinion on the financial statements.

Many small and medium-sized businesses get stuck at this point for one simple reason: they submit documents that are still incomplete, forcing quality control and review teams to work on versions that keep changing. This prolongs the process and leads to a flood of requests for clarification.

The shareholders' meeting is the final decision-making body. Its role is to approve the financial statements based on the documentation provided by the company.

However, the general meeting is not the place to resolve issues that should have been addressed beforehand. If members receive unclear or late materials, the meeting can turn into a tense situation rather than a moment of informed approval.

The most useful way to interpret this is from an organizational perspective. The process resembles an assembly line:

When an organ receives its information packet late, it doesn’t just slow down its own activity. It causes the entire subsequent flow to be delayed.

True efficiency, therefore, does not depend on a single “skilled” individual. It depends on coordination among different individuals, each with a unique role that cannot be replaced.

The process is more rigid than many small and medium-sized businesses realize. And it is precisely this rigidity that makes it manageable, if approached as a structured sequence rather than a task to be rushed through at the last minute.

The steps are strictly defined: 1) the directors prepare the draft financial statements within approximately one quarter of the end of the fiscal year, for example by March 30, 2026; 2) the draft is sent to the auditors several weeks before the shareholders’ meeting; 3) the auditors’ report is ready well in advance; 4) all documents are filed with the company’s registered office a certain amount of time before the shareholders’ meeting. In the same context, Infocamere IT 2025 data indicate that 92% of limited liability companies (SRLs) approve their financial statements within 120 days, while the Ministry of Economic Development (MISE) recorded approximately 8,500 appeals in 2024 due to errors in assessment, as reported in the analysis of financial statements, approval, and challenges.

The lesson is clear. Most companies manage to meet their standard deadlines. The most costly problems therefore do not stem from a lack of time in the abstract, but from errors in preparation and assessment.

The directors prepare the draft financial statements and the necessary supporting documents. Much of the final quality is determined at this stage.

If your team is still working with inconsistent financial statements, it may be helpful to consider reclassifying the balance sheet, as many issues with interpretation and reconciliation stem precisely from inconsistent reporting structures.

Here, the process takes on a different character. It is no longer just a matter of generating data, but of making it verifiable. Any inconsistency, missing documentation, or unclear criteria slows down the process.

This provision safeguards shareholders’ right to information. It is not a mere formality. If the documents arrive at the company’s offices when the timeframe is already tight, the company’s decision-making process suffers.

The notice of meeting must comply with the terms and provisions of the bylaws. The meeting, in turn, must make decisions based on complete and understandable materials.

The final phase brings the cycle to a close. It is the moment when approval moves beyond the company’s internal sphere and is formally established.

Many business owners focus on the penalty, but this approach is misleading. The more serious problem is that a delay in the approval process signals to shareholders, banks, and business partners that the company does not have its data under control.

A misjudgment doesn’t just come at a legal cost. It can lead to weeks of corrective work, discussions with outside professionals, postponements of the meeting, and a general slowdown in decision-making.

The budget approval process should not be viewed as a checklist of requirements. It should be viewed as a chain of accountability. Any weak link becomes a reputational and operational risk.

Penalties do exist, but they are not the heart of the problem. Focusing solely on the fine leads to underestimating the damage that a delay can cause to the company’s operations.

The financial impact of delays goes beyond civil penalties, which range from €137.33 to €1,376, as highlighted in the in-depth analysis of penalties for failure to approve the budget. Failure to approve the budget can trigger provisional management measures, limiting access to credit and the distribution of dividends. For SMEs that rely on short-term financing, this suspension can cause operational paralysis, with opportunity costs and bank penalties exceeding administrative penalties.

A management error often precedes a penalty. There are three particularly insidious ones.

A company that fails to successfully approve its financial statements sends a signal of uncertainty. This can have a negative impact on:

The most logical solution is not to “rush” at the end of the fiscal year. It is to address the root causes of the delay in advance: data opacity, fragmented manual checks, and the lack of a single view of progress.

If management treats the approval of financial statements as a risk management process, priorities shift as well. The question is no longer simply whether the documentation will arrive on time. Instead, the question is whether the company is capable of consistently generating, verifying, and explaining the data.

The most resilient SMEs aren’t the ones that “hold out until the final stretch.” They’re the ones that avoid getting into a crisis situation in the first place.

The most common cause of delays is rarely a single oversight. More often, it is a lack of information that builds up over time. Disconnected reports, duplicate spreadsheets, data that varies depending on the source, and checks that rely on people’s memories.

The recurring causes of non-approval in SMEs are not merely organizational; they stem from information gaps. The main ones are: lack of visibility into accounting data until the last minute, absence of automated compliance checklists, and prolonged audit cycles. Analytics platforms can prevent these issues with real-time dashboards and automated alerts, transforming approval from a critical event into a controlled process, as noted in the analysis dedicated to financial statement non-approval and liability profiles.

This observation is crucial for anyone running an SME. The bottleneck isn’t just regulatory; it’s informational.

A data-driven approach does not replace corporate bodies, the auditor, or the accountant. It enables them to work with data that is more transparent and less volatile.

In practice, an analytics platform can support the process by:

Those who are also considering complementary planning and monitoring tools may want to explore management control software, as financial oversight improves when management control and financial closing are integrated rather than treated as separate processes.

The biggest benefit isn't just the time saved. It's the reduction in uncertainty.

With data organized throughout the year, management can create a practical checklist:

For teams looking to standardize the production of preliminary reports, the report builder is a useful starting point, as it allows you to transform diverse datasets into readable and reproducible reports.

The most important benefit of automation isn’t that it “does the accounting for people.” It’s that it gives people time to focus on exceptions, rather than having to deal with the same recurring problems over and over again.

A good checklist is no substitute for technical expertise. However, it prevents the process from relying solely on people’s memories or the pressure of the final week.

Make sure that each recipient receives the documents at the right time. Delays often arise when a file is “almost ready” but isn’t actually usable yet.

Reread the document as if you were a third party. If an auditor, a partner, or a bank were to ask a question about a particular item, can the answer already be found in the available documents?

This final step should not be treated as a minor administrative task. Filing concludes the process and requires the same level of attention as the previous steps.

If a checklist seems excessive to you, it’s often a sign that the process relies too heavily on informal practices.

If the company is prepared, the documents are not merely in place. They are consistent with one another, legible to those who need to review them, and available well in advance. When these three conditions are not met, approval of the financial statements remains formally possible, but becomes operationally fragile.

The approval of the financial statements is much more than just a legal requirement. It demonstrates whether your company is able to close out its fiscal year in an orderly, transparent, and well-controlled manner.

The rules are clear. The roles are defined. The risks, however, go beyond mere penalties. The true cost of delays is felt in operational finances, in stakeholder relations, and in the time that management takes away from strategic decisions to deal with avoidable problems.

That is why the key question is not just “How do I comply with the regulations?” It is “How do I establish a process that ensures I am fully prepared?” When data preparation becomes an ongoing process, the financial statement approval process ceases to be a time of crisis and becomes an indicator of the company’s maturity.

This content is for informational purposes only and does not replace legal, corporate, or tax advice tailored to a specific case.

If you want to bring more control, clarity, and speed to the data preparation process leading up to the approval of the financial statements, discover ELECTE, the AI-powered data analytics platform designed to help SMEs transform fragmented data into reports, insights, and more informed decisions.

.svg)

.svg)

.svg)