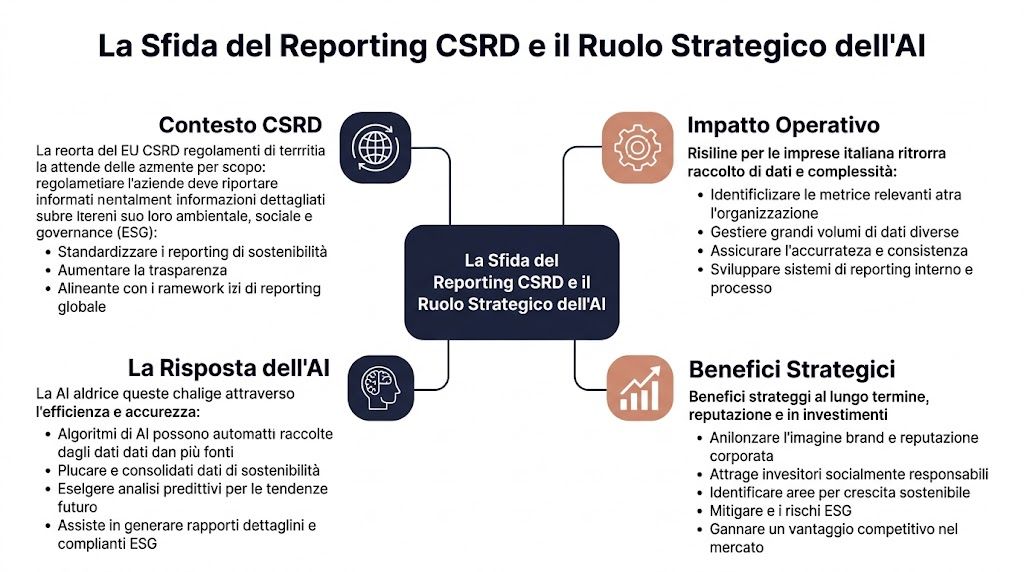

The most underestimated aspect of the CSRD isn’t writing the report. It’s the operational machinery required to get there. The directive requires reporting on over 1,000 data points, and for a manufacturing company with 500 suppliers, this can translate into analyzing 1,500–2,000 documents per cycle (market analysis on AI-driven ESG reporting automation). For a CFO, this means one simple thing: the problem isn’t just regulatory—it’s operational.

The good news is that AI is becoming a practical tool for managing this complexity. An AI-driven methodology for CSRD reporting can reduce manual data collection time by up to 70% and increase data processing accuracy to 95%, compared to 78% for manual processes, provided the source data is adequate (practical guide to using AI for CSRD audits). The bad news is that many Italian companies underestimate the pitfalls: scattered data, weak controls, models that are difficult to explain, and insufficient governance.

If you’re considering AI-powered CSRD reporting automation, the point isn’t just to buy a platform. The point is to build a process that can withstand audits and meet deadlines while ensuring data quality. Here’s a realistic guide, written with the same approach I’d use with a CFO: clear processes, explicit trade-offs, concrete benefits, and risks to manage before they become a problem.

For many Italian SMEs, the challenge isn’t understanding that the CSRD requires more data. The challenge is producing data that can stand up to an audit, with closing timelines that align with the finance team’s workflow, without creating a proliferation of files, reconciliations, and uncontrolled versions.

The challenge is compounded by the fact that CSRD reporting brings together a wide variety of sources. ERP systems, procurement data, HR records, utility bills, environmental data, supplier questionnaires, PDF documents, and methodological notes must all be integrated into a single, verifiable, and repeatable process. If this step remains manual, the CFO loses visibility precisely where the risk is highest: data quality, operational accountability, and the traceability of corrections.

In medium-sized companies, I often see the same pattern. The finance team coordinates reporting, but a significant portion of the information remains scattered across departments, external consultants, and suppliers. The result isn’t just delays. It’s a weak chain of control.

The typical signs are as follows:

Most CSRD issues don’t arise in the final report. They arise months earlier, during the data collection and cleaning process.

For an Italian SME, this issue is more critical than it is for large corporations. Structures are leaner, systems are less integrated, and methodological oversight often depends on just a few people. If one of these people changes roles or leaves the company, the process is immediately weakened.

AI is particularly helpful for high-volume, low-standardization tasks. It can classify documents, extract data from diverse sources, suggest associations between data points and ESRS requirements, flag anomalies, identify missing values, and generate narrative drafts consistent with the available data.

However, it works well only if it operates within a well-defined framework. Without a clear map of sources and responsibilities, even the best AI engine will amplify errors, ambiguities, and inconsistencies. That is why the priority is not the tool itself, but the structure of information flows and data sources related to CSRD reporting.

In practice, automation makes sense when it reduces repetitive work and increases human control over critical steps.

| Area | Risks in the manual process | Useful Applications of AI |

|---|---|---|

| Collection | missing inputs and constant delays | document capture and classification |

| Normalization | different file formats and incorrect conversions | standardization of fields, units, and structures |

| Check | late and incomplete audits | Alerts for anomalies, gaps, and inconsistencies |

| Audit trail | scattered evidence | link between data, source, and audit steps |

What’s needed here is realism. An AI system that generates a plausible number but fails to clearly explain which document it drew it from, what logic it used to transform it, and who validated it, creates a new problem instead of solving an old one.

In auditing, the question isn’t whether the output “looks correct.” The question is whether the process leading to that output can be reconstructed. This is the crux of the black box. If the team cannot demonstrate the data’s source, the rules applied, any exceptions that arose, and the final approval, the defensibility of the reporting is compromised.

That is why I always recommend treating AI as a pre-processing and verification tool, not as a substitute for professional judgment. The responsibility remains with the organization. This is particularly true for Scope 3, double materiality, and narratives based on estimates or methodological assumptions.

The real benefit isn't simply "getting the report done faster" in a general sense. It's about reducing three specific risks:

If these three outcomes are not materializing, the company is not improving its CSRD reporting. It is merely adding technology to a process that remains fragile.

In my experience, CSRD automation projects in Italian SMEs fail more often due to unmanaged data than because of limitations in the chosen platform. The point isn’t to simply add AI to the existing process. The point is to build a workflow that can withstand scrutiny, with verifiable steps and clear accountability.

The first decision concerns the scope of the data. We need to identify which ESRS data points are relevant to the company, which systems they are currently stored in, what data is missing, and who is responsible for validating them. Without this overview, automation can actually lead to more errors.

For an Italian SME, the challenge is not merely technical. Environmental, HR, and supply chain data are often scattered across ERP systems, Excel spreadsheets, supplier portals, and PDF documents. AI can help categorize these sources and establish an initial link between regulatory requirements and available data, but the responsibility for confirming that link remains an internal one.

The output at this stage is an operational matrix with six fields:

If this matrix is incomplete, the risk is not merely theoretical. During an audit, it becomes difficult to explain why a metric was included in the report with that scope and from that source.

The choice of platform should be based on internal control considerations, not just productivity. A well-done demo isn’t enough. It’s important to determine whether the system tracks transformations, retains versions, manages permissions, and provides a clear trail from raw data to the final output.

For a CFO, there are four key questions to ask the vendor:

It’s also worth looking into the issue of application connections right away. A platform that’s poorly integrated with business systems leads to manual reconciliations, frequent exceptions, and longer closing times. That’s why it’s a good idea to check the quality of the connectors to key business data sources in advance.

This is where the issue of the "black box" comes into play. If the vendor cannot demonstrate how the model classifies a document, flags an anomaly, or generates a narrative draft, the problem will surface later on—usually at the worst possible moment.

This is the stage where many projects lose credibility. AI can process large volumes of data quickly, but it cannot automatically correct inconsistent coding, differing units of measurement, misaligned scopes, or files uploaded using different logic from department to department.

There are three areas that need to be monitored:

This presents a real trade-off. The more you automate data entry, the more you need to invest in quality controls upstream. If you don’t, the finance team ends up having to validate exceptions generated by the system instead of reducing manual work.

A rule of thumb can help prevent configuration errors. Every automated workflow should include a reconciliation check that is understandable to someone without a technical background. If the check is only clear to the person who configured the platform, the process remains vulnerable.

Once the data streams have been cleaned, AI can deliver tangible value. It can flag anomalies, draft text, and assist with filling out repetitive sections. However, it is not advisable to rely on the model for the most sensitive aspects, such as methodological assumptions, consolidation scopes, or explanations of estimates and data gaps.

The most reliable methods are as follows:

In SMEs, the hidden risk is an overreliance on well-written output. A polished text can mask a weak factual basis. That’s why I always ask that two things be verified before approval: where each statement comes from, and which rule led the system to generate it.

Going live doesn’t mark the end of the project. It marks the beginning of a phase in which the automation system must prove its reliability month after month, as it handles new data, real-world exceptions, and changes to models or templates.

A basic governance framework should clarify the following points:

| Scope | Request to be closed |

|---|---|

| Ownership | who approves the data prior to disclosure |

| Exceptions | Who decides when an anomaly is acceptable? |

| Versions | which version of the data is included in the report |

| Audit trail | where the evidence is kept |

| AI Model | When updates are made and who approves the changes |

In smaller companies, operational risk is often concentrated in the hands of just a few people. If only one department is familiar with the rules, exceptions, and upload logic, automation remains dependent on individual memory. This is not a structural improvement.

A well-executed implementation yields three measurable outcomes: fewer manual corrections, fewer disputes during audits, and more predictable closing timelines. If any one of these three elements is missing, it is advisable to review the process design before expanding the use of AI.

Before investing in automation, it’s a good idea to conduct an internal maturity assessment. You don’t need an enterprise-level infrastructure. What you need is clarity on what you have, what’s missing, and what shouldn’t be delegated to the platform.

The right question isn’t “Do we have a lot of data?” It’s “Do we have traceable, consistent, and well-managed data?” If the answer is unclear, automation needs to be better prepared.

Check the following points:

A solid starting point doesn’t mean perfection. It means that every piece of important data has at least one owner, a recognizable source, and a validation criterion.

Many projects stall for reasons that aren't technical. The platform is in place, but no one defines its scope, approves new hires, or resolves conflicts between departments.

Organizational planning requires at least four clear decisions:

A CSRD project works when the company decides who is responsible for the data—not when it implements a new technological layer.

For an SME, the most effective model is often a hybrid one. Robust automation for data collection, classification, and consistency checks. Human oversight for decisions regarding scope, materiality, narrative, and final approval.

Automation makes sense when it changes the way we work on a daily basis. Retail and finance are two sectors where this is immediately apparent, though for different reasons.

In the Italian retail sector, the supply chain is often the bottleneck. Double materiality assessments suffer when impact data arrives in formats that are difficult to read or not comparable. A report cited by Deloitte indicates that 52% of Italian retail SMEs do not have granular impact data, and this is precisely where AI can accelerate benchmarking—though care must be taken to account for biases caused by weak supply chain data (double materiality analysis and AI).

In practice, a well-designed retail workflow follows this logic:

The useful output isn’t just the final number. It’s also the list of exceptions, the quality of the sources, and the trail of assumptions. That’s what really helps during the review process.

When it comes to storytelling, many companies realize too late that knowing how to analyze data isn’t enough. They also need to present the results in a way that’s easy to understand. The Data Storytelling Academy’s guide on how to write an effective report is particularly useful in this regard, as it helps transform a set of technical findings into a report that’s accessible to management, auditors, and stakeholders.

In finance, the process is different. The challenge isn’t just tracking physical or supply data, but linking risk, exposures, internal policies, and disclosures in a coherent manner. Here, AI is particularly useful for classifying material issues, analyzing qualitative inputs, and preparing drafts that the compliance team can refine.

A typical workflow includes:

| Phase | Tangible results |

|---|---|

| collection of internal feedback | inventory of material ESG risks |

| document analysis | Summary of policies, controls, and gaps |

| classification | Disclosure Topic Map |

| human review | Approval of scope and language |

| reporting | narrative sections and control dashboards |

In finance, the benefit isn’t “typing faster.” It’s about reducing discrepancies between departments that produce the same data using different definitions.

For an SME, the challenge isn’t finding yet another platform to add to the stack. The challenge is integrating data, controls, and outputs into a workflow that the team can actually use.

ELECTE, an AI-powered data analytics platform for SMEs, is valuable in this context because it covers the entire process. It connects diverse data sources, pre-processes the data, makes it easier to identify anomalies, and transforms complex datasets into insights that even non-technical users can understand.

In the context of the CSRD, this approach is particularly helpful in three key areas:

For the final disclosure phase, the ability to generate clear and reusable outputs is particularly important. The logic behind a report builder designed to create automated and customizable reports is precisely what is missing in many CSRD processes that are still managed using disconnected documents, parallel versions, and delayed consolidations.

The right platform does not replace management judgment. It eliminates the repetitive work that prevents management from exercising that judgment effectively.

This is where an analytics-first approach makes all the difference. It doesn’t treat reporting as a final document to be laid out, but as the natural outcome of a data process that is more organized, more transparent, and easier to manage.

The adoption of AI in sustainability reporting does not fail because the technology is immature. It fails when a company assigns it tasks that require judgment, context, or explanations that the model cannot provide on its own.

In Italy, the lack of transparency in AI is a barrier for 62% of SMEs that must comply with the CSRD, and in similar contexts, 28% of audit rejections are due to non-explainable models (study on AI and sustainability reporting for SMEs). This figure should be carefully considered. The risk is not that “AI makes mistakes.” The risk is that “the company cannot explain how it arrived at that conclusion.”

The practical countermeasures are very concrete:

For many CFOs, this issue is also linked to broader regulatory governance. It is worth keeping in mind the compliance framework and requirements of the European AI Act, as the direction of European regulation is clearly moving toward greater transparency, more oversight, and less blind reliance on non-interpretable models.

The other pitfall is more mundane, but often more damaging. If the data is of poor quality, automation simply speeds up an existing error. This happens especially with non-standardized supplier documents, misaligned scopes, and differing definitions across departments.

The most effective defenses are practical, not theoretical:

| Risk | Practical mitigation |

|---|---|

| incomplete data | Mandatory field rules and exception handling |

| inconsistent units | centralized standardization |

| multiple versions | a single source of truth for each disclosure |

| unsubstantiated claims | requirement to provide supporting documentation |

The model that works best is still the human-in-the-loop approach. The AI collects, classifies, flags, and prepares the data. The team validates, interprets, and approves it.

Yes, but within certain limits. AI is useful for reading PDFs, open-ended questionnaires, attachments, and non-standard documentation. It works well when it needs to extract fields, recognize recurring categories, and flag missing information. However, it is not enough on its own to ensure that the data is accurate within the CSRD framework. You must always include validation rules and a human review of exceptions.

It remains a central role. AI does not determine materiality, scope, methodologies, or final assumptions in place of the company. The finance and compliance team defines rules, approves exceptions, ensures the consistency of disclosures, and verifies that the report reflects the actual operating model. The auditor, in turn, needs a paper trail, evidence, and verifiable steps.

When AI is incorporated into reporting, human oversight doesn’t disappear. It becomes more important and more focused.

More than many SMEs realize. Total rigidity isn’t necessary, but some basic standards are required. Consistent file names, required fields, data ownership, approval rules, and a well-organized document repository. Without this discipline, automation remains incomplete.

Yes. When the process is well-established, the data collected for the CSRD also becomes useful for procurement, risk management, management control, and engagement with investors or customers. The real benefit isn’t just “producing the report.” It’s having a better data foundation for better decisions.

No. It’s generally best to start with the most critical and repetitive workflows. For example, collecting data from suppliers, cross-departmental reconciliations, or drafting narrative disclosures that require frequent updates. The mistake is trying to automate everything at once without first establishing governance rules.

Focus less on the demo and more on the process. Ask whether the platform keeps a record of transformations, handles exceptions, links outputs to sources, can be used by non-technical users, and integrates with the systems you already have. A credible solution for CSRD reporting should help you work more effectively, not just generate documents faster.

If you want to turn CSRD compliance into a more organized, traceable, and business-friendly process, find out how ELECTE can help you connect data sources, automate reports, and gain clear insights without enterprise-level complexity.

.svg)

.svg)

.svg)